The business in India has always been impacted by the complex tax structures, which acted as a deterrent for planning efficient business operations. Every state has imposed its own set of rules and taxes on the business holders. The lack of clarity on the tax structure has resulted in a chaotic tax environment for the business industry.

The business in India has always been impacted by the complex tax structures, which acted as a deterrent for planning efficient business operations. Every state has imposed its own set of rules and taxes on the business holders. The lack of clarity on the tax structure has resulted in a chaotic tax environment for the business industry.

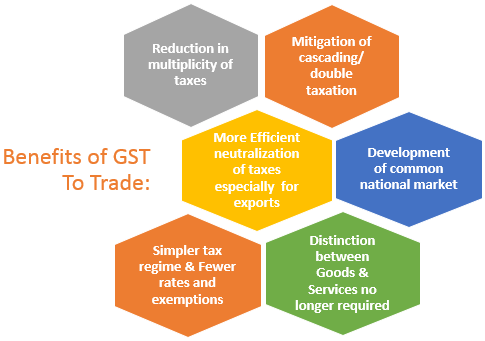

The introduction of Goods and Services Tax (GST) will mark a significant move in the field of tax reforms in India. By amalgamating major Central and State taxes into a single tax class, it would abolish double taxation in a simpler way and object the creation of a common national market. GST will replace all indirect taxes levied on goods and services by the Central and state governments.

As GST would be applicable on “supply” of goods or services as against the present concept of tax on the manufacture of goods, sale of goods and provision of services, same will lead to many benefits not only for the consumers in terms of a reduction in the overall tax burden on goods, which is currently estimated to be around 25%-30% but also it will mark significant leads in Trade.

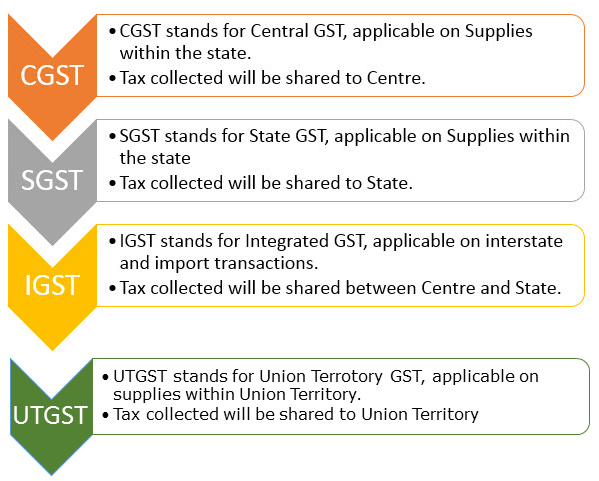

GST will be categorized in two components with State and Centre as separate stakeholders. Components of Dual GST:

GST will be categorized in two components with State and Centre as separate stakeholders. Components of Dual GST:

Out of 7 Union Territories*, UTGST is applied on only 5 of them, however, SGST can be applied in Union Territories such as New Delhi and Puducherry, since both have their individual legislatures, and can be considered as “States” as per GST process.

Out of 7 Union Territories*, UTGST is applied on only 5 of them, however, SGST can be applied in Union Territories such as New Delhi and Puducherry, since both have their individual legislatures, and can be considered as “States” as per GST process.

E-commerce organizations (Sellers & Marketplaces) are looking forward to the implementation of GST expecting high clarity, and dismissal of state specific rules and multiple Taxes.

*List Of 5 Union Territories considered under GST:

- Andaman and Nicobar

- Lakshadweep

- Dadra and Nagar Haveli

- Daman and Diu

- Chandigarh

Sellers and Marketplaces have to meet basic requirements to run business post GST implementation.

Below are the mandatory requirement from Sellers and marketplaces which will be implemented in Uniware to help sellers in smooth and issue free order processing from 1st July, 2017:

1- GST Number/ Registration:

All sellers mandatorily require to register under GST. So now even e-commerce sellers whose aggregate turnover does not exceed the threshold limit for registration will still have to compulsorily register to sell online.

Key Points for Registration:

- If a seller has business with same PAN in different states is now expected to register separately for each of the States where he has a business operation.

- If a seller has two business verticals in a state, he/she may obtain a separate registration for each business vertical.

- If seller has two different businesses with two TIN numbers in the same state, he can have common GST registration for both.

As per this mandatory requirement, seller has to update GST No. in Facility, Billing Party, Customer and vendor for order processing from 1st July in Uniware. Validation of GSTIN will be done using state code & PAN rules which will be already stored in backend to validate the GSTIN filled by the supplier.

2- HSN Number:

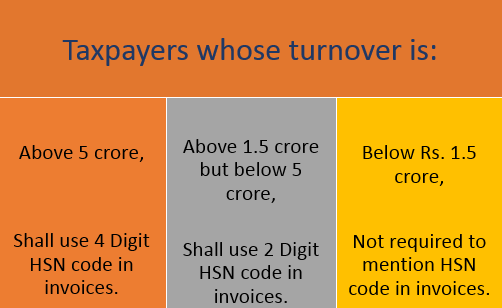

HSN Code stands for Harmonized System Nomenclature. HSN number is mainly used for classifying goods to compute Value Added Tax in India. Now, same classification code (HSN) is adopted for classifying Goods and Service Tax for GST as well.

Under GST, the HSN code would be utilized by a taxable individual for classification of goods , but the format of HSN code will be based on the taxpayer’s turnover. When preparing Tax Invoice for GST, the HSN number must be mentioned on GST Tax invoice and also to be declared while filing the GST returns.

To mention HSN codes for the products will also become mandatory for sellers in Uniware as well. Same information will be saved under item type (products) created in Uniware.

To mention HSN codes for the products will also become mandatory for sellers in Uniware as well. Same information will be saved under item type (products) created in Uniware.

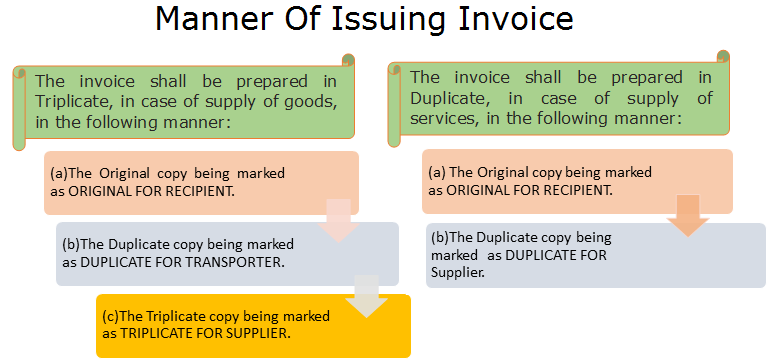

3-Issue of Tax Invoice Under GST:

Every registered person is required to issue a tax invoice at the time of supply of taxable goods/services and the invoice shall contain following particulars:-

Supply of Goods/Services

- Description of goods/services;

- Quantity of goods;

- Value of goods/services;

- Tax charged on Value of goods/services; and

- Such other particulars as may be prescribed.

Further the invoice shall be prepared in triplicate, in case of supply of goods and duplicate in case of supply of services. Uniware will provide all above required changes and number of invoices as per supply of goods through its portal.

Below mentioned is the detailed information for the way of issuing Invoice after GST is implemented, which will be provided by Uniware as well. Invoices generated through Uniware will also have the prescribed format as described above.

Note: Fetching of Marketplace Invoices:

Note: Fetching of Marketplace Invoices:

Unicommerce would not only provide GST ready invoice templates for both B2B and B2C transactions, but also overhaul the architecture to fetch invoices from marketplaces, instead of pushing the invoices to marketplaces, wherever required. For example, Unicommerce is moving to the new version of APIs in case of Flipkart to be able to fetch their invoices, as well as pass on the HSN code to the marketplace etc. to comply with the GST regime.

4- Credit Note:

Credit note will be reflected in the monthly return in which such notes have been issued.

When a Credit note should be issued:

When a registered dealer issues a tax invoice and in these invoices the tax amount is greater than the tax return filed for that period, seller has to issue credit note to the partner business owner containing such particulars as may be prescribed.

In Uniware as well, credit notes will be provided for Sale Order, Inter-state Gatepass and purchase order returns in the prescribed format set by Government bodies.

For returns filing post July 1, 2017 credit note is required only if GST was applied on the corresponding invoice.

5- Return filing Process Under GST:

Monthly billing will constitute filing of all below mentioned forms on prescribed dates:

- Form GSTR-1: Upload all invoice-wise details of supplies to registered taxable persons and aggregate value of supplies to unregistered persons made through the e-commerce platform must be provided. (By 10th).

- Form GSTR-2A: The aggregate amount of tax collected by e-commerce operators (Tax collected at Source or TCS)** in the previous month will be auto populated, based on Form GSTR-8*** filed by the e-commerce operators. (On 11th).

- Form GSTR-2: The details of tax collected by the e-commerce operator can be accepted or modified in Form GSTR-2 (On 15th).

- Form GST ITC-1: Any discrepancy in supplies furnished with supplies reported by the e-commerce operator is made available to a supplier. The discrepancy must be rectified in the return for the month in which it is communicated.If not rectified and the value of supplies furnished by the operator is more than the value furnished by the supplier, the differential amount along with interest will be added to the tax liability of the supplier for the succeeding month.(On 21st).

**tax collected by e-commerce operators (Marketplaces) – Every e-commerce operator should collect tax @ 2% of net value of taxable supplies, out of payments to suppliers (sellers) supplying goods or services through their portals.

| Net value of taxable supplies = Value of taxable supplies made by all registered taxable persons through the marketplace, other than notified supplies on which tax is paid by the marketplace (-) Value of taxable supplies returned to the sellers. |

***GSTR-8– Form GSTR-8 will be filed by every e-Commerce operator (marketplace), who is required to collect tax at source (TCS) under GST electronically through the https://www.gst.gov.in/.

6- Compensation Cess-

A new cess with the name “GST Compensation Cess” for first 5 years on some specified items will be implemented which will be credited to the GST Compensation Fund. The need for this cess rise to compensate the manufacturing states, as GST is a destination cum consumption based tax, so in order to compensate states from this kind of probable loss this will be implemented along with CGST, SGST and IGST.

Refer below link to know the Compensation Cess rates defined by government as defined in Central Board of Excise and Customs: CBEC-Compensation Cess

Uniware will reflect this cess as on the Invoices as well.

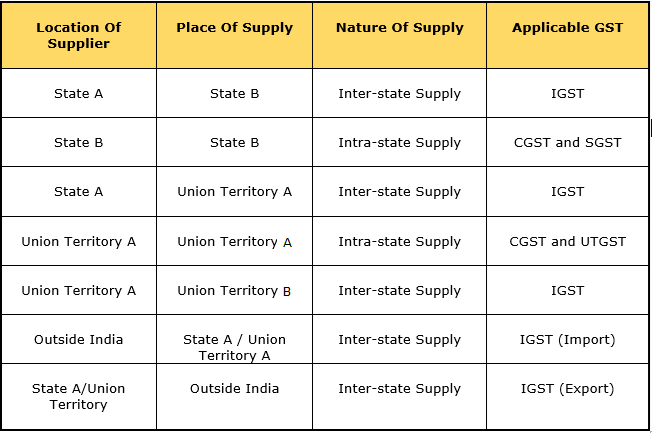

7-Tax Calculation as per consumption of Goods supplied by Supplier Under GST:

Refer below table reflecting the tax to be calculated as per location of supplier and place of Supply, we have tried to cover all possible conditions containing all the calculations:

Note: Go Live date for these changes will be (Jul 1, 2017) in Uniware and if prepaid order is received on Jun 30 invoice is printed on Jul 1, GST will not be applied in this scenario. However, if same order will be COD, then GST will be applied.

Note: Go Live date for these changes will be (Jul 1, 2017) in Uniware and if prepaid order is received on Jun 30 invoice is printed on Jul 1, GST will not be applied in this scenario. However, if same order will be COD, then GST will be applied.

8- Impact of GST on Warehouse Management Processes:

GST regime will not only affect the e-commerce operators and the sellers but will also have important effects on warehousing management processes.

As per current tax regime, there is no uniformity and ease in tax implementation across various warehouse management, logistics and supply chain management processes. Effect of taxation at every step of these processes majorly affect the utilization of available resources. In present scenario, the location of warehouse is generally chosen to evade the taxes and reduce the logistics costs.

With GST, warehousing processes will also become uniform with the introduction of common market for Goods and services, breaking the state barriers and borders. This will lead to reduction in number of warehouses, and more organized warehouses enhancing the overall efficiency.

Unicommecre’s warehouse management software, Uniware is also ready to handle all warehouse processes such as inbound, outbound etc. as per new GST rules. All such changes will reflect in intra state/ interstate transfer documents, such as Gatepass.

To sum up, the below table describes the compliance requirements for GST regime and how Uniware will help the sellers in incorporating the changes at their end:

Conclusion:

Conclusion:

Conclusion:

Conclusion:Taxation on e-commerce transactions in the current regime is confusing as different states have different levies of tax and there is no clarity on Taxes levied on goods and services. The GST regime will now bring uniformity in the taxation process for e-commerce platforms and sellers.

- Seamless availability of input credit will result in reduced cost of operations for suppliers such as warehousing, logistics, marketplace commission, etc. as they will now be able to take the credit of tax paid on inputs, which was until now adding up to their cost.

- Unified common national market in India for the goods and services, regardless of whether they are sold at physical stores or online. GST will bring greater access to the customers across the nation for sellers.

- Prevent cascading of taxes as Input Tax Credit will be available on goods and services at every stage of supply.

- Simplified and automated procedures for various processes such as registration, returns, refunds, tax payments, etc.

As a supplier, it is important to plan for the GST regime. Awareness of the compliance requirements under GST like registration for GST number, documentation, filing of returns etc., planning and preparation for entering into GST module of taxation will ensure that suppliers can capitalize on the new era of e-commerce in India.